Don't Fear the Taxman: BIK Guide 2022

Ireland’s #1 Mileage App

ALLY MILEAGE

60-Second Video | 30-Day Free Trial | Review | Testimonials

Update: Read our 2024 Company Car / EV BIK Guide here

INTRODUCTION

There are many good reasons why employers choose to offer staff company cars - such as attracting and retaining key talent or to minimise vehicle risk. Unfortunately, this important benefit also comes with a Benefit-In-Kind (“BIK”) Tax which employers need to measure and manage appropriately. DriverFocus has researched current best-practice around tackling business mileage and discussed the issues with Ireland’s leading tax and payroll professionals. In this guide, we share our findings and explain that with the lifting of Revenue’s Concession from 1st January 2022, why now is a really good time to review how you record and report business mileage.

REVENUE’S “CONCESSIONARY TREATMENT” FOR COVID-19 CIRCUMSTANCES ENDS

In response to the Covid-19 pandemic, it was necessary for Revenue to introduce some temporary Covid-19 measures in relation to the operation of BIK on employer-provided vehicles.

The business mileage performed by an employee each year is paramount to the determination of the taxable BIK which can range from between 6% and 30% of the Open Market Value of the vehicle (OMV) provided. Under the Covid-19 concessions available, Revenue allowed the BIK to be based on the business mileage performed in January 2020 in order to determine which percentage of the OMV is subject to BIK taxation. Without this concession, there would almost certainly have been a significant reduction in business mileage performed during that period and as a result, a higher BIK charge on the employee.

In their most recent update, Revenue has confirmed that this measure will apply for the 2020 and 2021 years of assessment. For 2022, Revenue has agreed that the measure will only apply for the period where there is a public health guidance requirement for all employees to work from home, unless it is necessary to attend the workplace in person. As such, Revenue advises “from 1 January 2022, where public health guidance no longer requires an employee to work from home, the BIK charge on an employer provided vehicle should be calculated in the ‘usual’ manner” - i.e. based on actual business mileage performed. This will be the case where an employer facilitates an employee in continuing to work from home or undertake limited or reduced business mileage after the relaxation of this public health guidance.

According to Claire Davey, Tax Director at KPMG, "as Ireland starts to reopen and restrictions are eased, employers should be mindful that they will need to calculate company car BIK in the normal manner and have processes are in place to ensure they are no longer relying on Covid-19 BIK company car concessions which are no longer available in practice".

THE CHALLENGE - REAL-TIME REPORTING NOW REQUIRED

From January 1st 2019, the Revenue Commissioners in Ireland have introduced major changes to the PAYE system. A key element of this modernisation programme is the need for employers to report PAYE in real-time. What this means in practice is that instead of a year-end reporting obligation, employers are now expected to submit a return each payday.

When it comes to company car BIK and business mileage reimbursement, Revenue advise employers that:

"You will need to calculate the ‘cash equivalent’ of your employee’s private use of the company car. The cash equivalent is a percentage of the Original Market Value (OMV) of the car. The percentage is based on the amount of mileage for business purposes".

In 2019, PwC wrote about the new real-time reporting obligation in relation to company cars:

"Company cars are typically provided for the full year, and the distances for determining the applicable tax rate are based on the number of miles/kilometres driven in the calendar year. Many employers struggle to get their employees to maintain and submit accurate logs on a regular basis, with the result that the employer may include the highest BIK amount (or an estimate based on the prior year’s mileage) and then perform a true-up semi-annually or at year-end. Particularly for employers who process weekly or fortnightly payrolls, it would involve significant additional business process to request, obtain and review all employee mileage logs on a weekly/fortnightly basis."

In a more recent update, Revenue advised:

Accountancy firms with experience in this area, report that business mileage and BIK tax have consistently been among the top areas of interest when Revenue engage in what they refer to as “Timely Targeted Interventions”. With tapering relief on BIK tax for higher levels of business mileage, if anything, there can be a temptation for some individuals to claim more business kilometres than actually driven. Coupled with recently increased resources and REAP - Revenue’s compliance profiling system - it is anticipated non-compliance risks will be targeted earlier and more frequently.

Another consequence to note is that from 2019, there are also increased penalties for underpaid tax. For example, the fixed penalty of up to €4,000 per incorrect return, effectively means a potential penalty of €48,000 for any given year. This is in addition to statutory penalties which range from 3% to 100% of the tax due.

Finally, in cases where PAYE tax on mileage and travel expenses is not correctly withheld, the tax will be recouped by Revenue on a grossed-up basis, meaning that every €1,000 paid to employees will cost the employer €2,309 including tax and employer PRSI.

COMPANY CAR BIK EXAMPLE

Sam is an account manager and drives a company car with an OMV of €25,000. Suppose in 2019, Sam claimed annual business mileage of 28,000 kms and payroll applied reduced BIK tax of 24%. on the €25,000 of €6,000 instead of €7,500. However, when Revenue undertook an audit, Sam could not produce sufficient evidence of this business mileage and so the following tax and penalties were applied:

Underpaid tax: €1,500

Fixed penalties: €4,000

Statutory penalty: €750

TOTAL CHARGE: €6,250

Note: this example is based on just one driver, for one quarter and for one band change. Clearly the tax and penalties can be higher if any of these three conditions are increased.

Electric Vehicles (EVs)

Finance Act 2017 introduced an exemption from benefit-in-kind provisions in relation to electric vehicles. An electric vehicle is one that derives its motive power exclusively from an electric motor, as such hybrid vehicles do not qualify for this treatment. As Sustainable Energy Authority of Ireland (SEAI) grants are paid after the registration of the vehicle, the OMV is not reduced by the value of the SEAI grant.

Section 5 of the Finance Bill 2019 amends the current exemption for electric cars and vans with a market value of less than €50,000 in section 121 of the Taxes Consolidation Act 1997 by extending the exemption to 31 December 2022. For vehicles with an OMV above €50,000, the BIK in 2022 is calculated by reducing the OMV by €50,000. A new benefit in kind valuation for employer provided cars will take effect that will be based on kilometres travelled and the CO2 emission levels of the car in 2023.

HOW TO BE TAX COMPLIANT TODAY

Undertake a tax review to help identify potential gaps in your current processes, including any company car BIK tax and/or business mileage reimbursements for grey fleet drivers. You should speak with your tax advisor for guidance and/or see below for further best-practice guidance and contacts.

Ensure your BIK tax deductions follow Revenue rules, see Revenue’s BIK Ready-Reckoner for instance. Of course, Revenue are well aware that claimed business mileage logs submitted on Excel, may or may not reflect the reality of business trips undertaken i.e. whether trip distances are exaggerated or if the journeys occurred at all! As a consequence, Revenue audits invariably target company car BIK / business mileage expenses as a relatively easy way to show a return on tax audits. Not surprisingly, this practice was likened to “shooting fish in a barrel” by more than a few tax experts!

Simple to use digital technology can also help you ensure tax compliance by providing evidence of actual - rather than claimed - business trips in the form of an electronic logbook. Reducing the hassle of mileage administration for staff who are on the road, also means that they will have more time to spend on more productive activities. A third benefit is that payroll professionals - already facing an increased reporting burden - will not have to wait for or spend so much time chasing colleagues for their mileage logs.

Ireland’s #1 Mileage App

ALLY MILEAGE

60-Second Video | 30-Day Free Trial | Review | Testimonials

CHOOSING A BUSINESS MILEAGE SYSTEM

Today, most employees - more than 80% according to an IPASS Survey in 2017 - use Excel to report business mileage. Of course, such claimed mileage can include fictitious trips or “rounding-up”. There is though, a better way to ensure that your business is not exposed to additional costs and tax penalties as outlined above.

“In our view, the only “watertight” method of ensuring that the company car BIK is calculated correctly is to track business mileage by keeping a log book or using a smartphone app”

- Claire Davey, Tax Director, KPMG Ireland

While commercial vehicle telematics (commonly referred to as “trackers”) typically have some trip distance reporting functionality, these systems tend to be overly complex, expensive and viewed as “big brother” by staff and decision-makers who simply want Revenue-required, business trip logging. In contrast, smartphone app-based technology - such as DriverFocus ALLY- can automate actual business mileage capture while being a simple, positive and respectful experience from a user perspective. Whatever mileage capture system you implement should greatly help remove the “low-hanging fruit” the next time a Revenue Inspector comes calling. And of course showing strong compliance around BIK and mileage should lessen the chances of a more extensive Revenue intervention!

FURTHER GUIDANCE

Guidance:

IPASS - BIK Training for Payroll Professionals

Revenue - Guide on Private Use of Company Cars

Revenue - December 2021 update to include Electric Vehicles (EVs) (and Covid Concession)

Articles:

DriverFocus - COVID-19: Company Cars and BIK - What You Need to Know For 2021

Deloitte - article in Accountancy Ireland (January 2019)

KPMG - PAYE Modernisation and Real-Time Reporting

PKF - PAYE Modernisation and Benefit in Kind

PwC- PAYE Modernisation: Are you ready for real-time reporting?

Appendix - BIK Calculator for 2022:

Step One: Capture and verify Business Mileage (in kms).

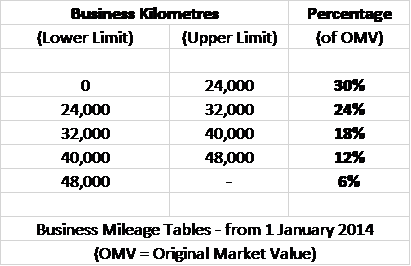

Step Two: Determine relevant BIK rate (from 6% to 30%) from Revenue table.

Step Three: Multiply OMV (original market value of the company car) by the relevant BIK rate

{kind=link}